Spotify: What's Baked In at $150?

And what would a reasonable base case suggest the stock is worth?

I shared some qualitative thoughts about Spotify earlier this month in Spotify: A Compounding Effect. In this post, I’ll focus on the quantitative as it relates to valuation.

First, I’ll walk you through an update to my reverse DCF now that the stock has quietly more than doubled in the last five months. This tries to answer the question, “What’s baked in at $150?" or “What do we need to believe about Spotify’s future to earn average returns over time?”

Clearly, higher expectations are baked in at $150 per share than they were at $69 six months ago. But it would be hard to have a sense of what those expectations might be and how they’ve changed without running some numbers.

So here we go—what sort of future for Spotify is priced in at $150? I’ll share the model later in this post but here’s the gist of it:

Total MAUs grow from 515 million last quarter to 705 million in a decade and 815 million a decade beyond that. That’s a 2.6% average annual growth rate, sharply lower than the 20%+ growth rates of today.

Premium subs grow from 210 million last quarter to 285 million in a decade and 337 million a decade beyond that. That’s a 2.5% average annual growth rate. In both years, Premium sub penetration of total MAUs is about 41%, flat with today.

Premium ARPU grows at a 3.3% annual rate to reach €6.08 in a decade and €8.67 a decade beyond that. That implies a fairly modest amount of long-term pricing power—despite ad-free streaming music being clearly underpriced today—offset by some product and geographic mix shift to lower ARPU plans and regions.

Ad-Supported ARPU, which I define as ad revenue over average total MAUs, grows at a 4.5% average annual rate over time. I think the largest audio platform in the world should get an appropriate share of advertising revenue over time. This implies ad revenue gets up to about 16% of Spotify’s total revenue a couple decades out, which misses management’s 20%-40% long-term target range for ad revenue as a percent of total revenue.

With those assumptions, total revenue would grow from about €11.9 billion last year to €24.0 billion in a decade and €41.4 billion a decade beyond that. That’s a 6.4% average annual growth rate.

Incremental gross margins on the Premium side are 33.3% this year and then jumps to 38.0% next year and beyond partially due to a more favorable arrangement with the labels as it relates to sharing the upside from future price increases. That takes overall Premium gross margin into the low 30%s a decade out and mid-30%s another decade out.

Incremental gross margins on the Ad-Supported side are 30% this year, 40% next year, and 50% thereafter. That takes Ad-Supported gross margin into the high 20%s a decade out and into the high 30%s a decade beyond that.

Overall gross margin reaches 32.2% in a decade and 35.5% a decade beyond that. That is basically at or below the low end of the 35%-40% long-term gross margin range management has discussed.

Incremental R&D is 40% this year, drops to 8% next year, and 6% thereafter. As revenue grows, the R&D dollars would get silly if this line did not see leverage.

Incremental S&M is 13% this year, 7% next year, and 5% thereafter.

Incremental G&A is 3.0% this year and beyond.

With those assumptions, operating margin rises from slightly negative today to 8.3% in a decade and 15.8% another decade beyond that. With a 10% discount rate, a ~5% terminal year free cash flow yield, and a 1.073 EUR/USD exchange rate, and adjusting for the value of non-operating items, SPOT’s fair value is the current $150 stock price. I’ll let you be the judge of those assumptions and how achievable they might be for Spotify, but if that played out I’d expect SPOT holders would earn average long-term returns.

Base Case

Here are my base case assumptions in the same format:

Total MAUs grow from 515 million last quarter to 840 million in a decade and 1.044 billion a decade beyond that. That’s a 3.9% average annual growth rate, sharply lower than the 20%+ growth rates of today.

Premium subs grow from 210 million last quarter to 335 million in a decade and 428 million a decade beyond that. That’s a 3.8% average annual growth rate. In both years, Premium sub penetration of total MAUs is about 41%, flat with today.

Premium ARPU grows at a 4.4% annual rate to reach €6.69 in a decade and €10.62 a decade beyond that. That implies more realistic long-term pricing power given ad-free streaming music being pretty clearly underpriced today partially offset by some product and geographic mix shift to lower ARPU plans and regions.

Ad-Supported ARPU, which I define as ad revenue over average total MAUs, grows at a 7.1% average annual rate over time. I think the largest audio platform in the world should get an appropriate share of advertising revenue over time. This also implies ad revenue gets up to about 20% of Spotify’s total revenue a couple decades out, hitting the bottom end of management’s 20%-40% long-term target range for ad revenue as a percent of total revenue.

With those assumptions, total revenue would grow from about €12.6 billion this year to €31.6 billion in a decade and €67.6 billion a decade beyond that.

Incremental gross margins on the Premium side are 35.0% this year and then 40.0% next year and beyond due to Marketplace growth and a more favorable arrangement with the labels as it relates to sharing the upside from future price increases. That takes overall Premium gross margin to 35.1% a decade out and 37.6% another decade beyond that.

Incremental gross margins on the Ad-Supported side are 30% this year, 40% next year, and 50% thereafter. That takes Ad-Supported gross margin to 35.5% a decade out and to 44.4% a decade beyond that.

Overall gross margin hits 35.2% in a decade and 39.0% a decade beyond that. This is consistent with the 35%-40% long-term gross margin range management has discussed.

Incremental R&D is 40% this year, drops to 8% next year, and 6% thereafter. As revenue grows, the R&D dollars would get silly if this line did not see leverage.

Incremental S&M is 13% this year, 7% next year, and 5% thereafter.

Incremental G&A is 3.0% this year and beyond.

With those assumptions, operating margin rises from slightly negative today to 21.3% two decades out. With a 10% discount rate, a ~5% terminal year free cash flow yield, and a 1.073 EUR/USD exchange rate, and adjusting for non-operating items, SPOT’s fair value is $315 per share, more than twice it’s current trading price.

Obviously, it’s unknowable when or if the market might price in this scenario. But long-term investors who are willing to underwrite this and are proven right in the long run should earn very attractive long-term returns.

Say it takes 5 years for the market to come around to this view. In theory, the $315 per share valuation would grow at a rate close to the 10% discount rate. That would take the current valuation close to 61% higher to about $507. That implies a 3.4x in 5 years or a about a 27.5% average annual return. I’d take that!

Price Increase Negotiations

It seems fairly predictable that Spotify will announce a price increase in major markets, including the U.S., in conjunction with a more favorable revenue split with the labels. I wouldn’t be surprised if this caused an immediate 5%-10% pop in the stock or maybe more. After all, this would seem to break two prevailing narratives in the investment community. The first one is that Spotify is beholden to the labels and that wholesale transfer pricing will eternally prevent Spotify from increasing its margins (which seems already disproven to me given Marketplace’s success expanding music margins over time). And second, the narrative that Spotify doesn’t have pricing power because there’s too much big tech competition offering similar services. Both narratives seem like consensus views to me, so this news would seem to call both narratives into question.

Daniel has talked about it as if it might happen this year. Warner Music has acknowledged that something has to change to give the DSPs the incentive to raise prices. Streaming music is frustratingly low-priced for the labels but Spotify is not in a hurry to raise them without getting concessions. It seems like the winds are moving in Spotify’s favor on this topic.

Scenario Analysis

Here is the PDF of my scenario analysis and 6 DCFs that includes both of the above scenarios and a few others:

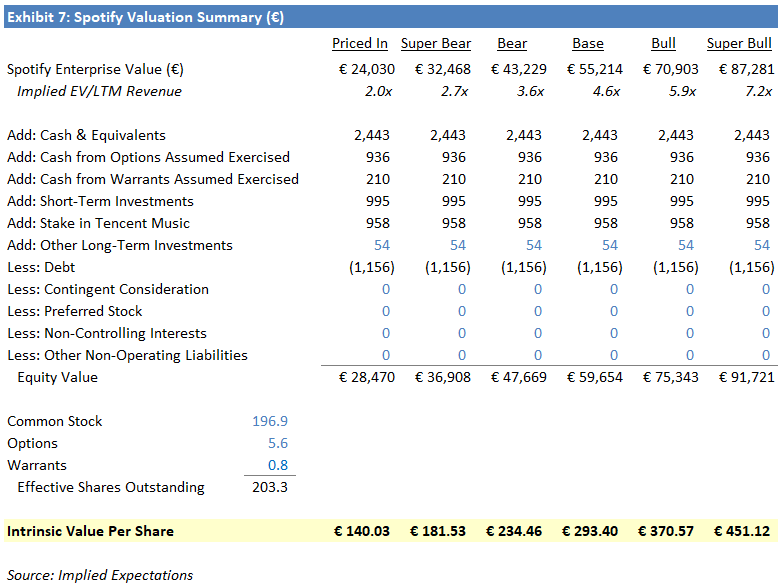

And here is the valuation summary exhibit that brings in the valuations derived in each scenario and adjusts for non-operating items. Here is is in Euros, Spotify’s reporting currency:

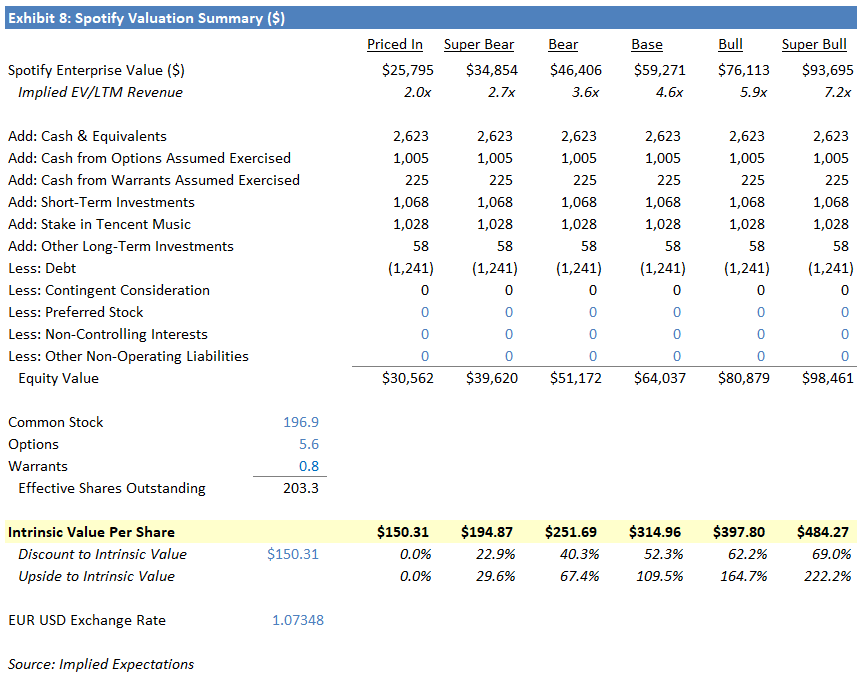

And in U.S. dollars, in which the stock trades:

Disclosure: Long SPOT

Disclaimer: This post is for entertainment purposes only and is not a recommendation to buy or sell any security. Everything I write could be completely wrong and the stock I’m writing about could go to $0. Rely entirely on your own research and investment judgement.

Great work as always IE!