[Note: This post was delayed because my Dad recently passed away. Thanks for understanding.]

I thought Spotify’s third-quarter report was pretty great. Here’s the third-quarter slide deck if you haven’t seen it.

User and subscriber growth continued to show impressive strength. MAUs grew 26% y/y to 574 million, adding 23 million sequentially and 2 million ahead of guidance. That was the company’s second-largest quarter ever for MAU net adds. Premium subs grew 16% y/y to 226 million, adding 6 million sequentially and 2 million ahead of guidance. Fourth-quarter guidance calls for more robust growth with MAUs reaching 601 million and Premium subs reaching 235 million. The long-term 1 billion MAU figure that has been thrown around for a long time no longer feels like a big stretch anymore.

As an aside, I’ve been building out my long-term scenario analysis for Spotify on a regular basis since early 2019. It’s interesting to look back and see how my assumptions fared versus what actually played out. In March of 2019, my Base case assumed:

Spotify would reach 433 million MAUs and 207 million Premium subs by the end of 2023. In contrast, the company should reach 601 million and 235 million, respectively, according to guidance.

Spotify would generate €11.3 billion of revenue in 2023. With just the current quarter to go, management’s guidance calls for €13.3 billion.

Spotify would generate €3.5 billion of gross profit in 2023, which is a 30.6% gross margin. Given fourth-quarter guidance, Spotify will reach €3.4 billion of gross profit, which is a 25.6% gross margin.

Spotify would spend €2.7 billion on opex in 2023, which led to about €700 million of operating income. It looks like opex this year will be closer to €3.7 billion, leading to a €300 million of operating loss.

In sum, Spotify handily beat my 4-year forward user, subscriber, and revenue estimates but underperformed on gross margin, opex, and therefore operating income and free cash flow. The gross margin underperformance is largely due to the Ad-Supported segment and specifically the podcasting business, which has been in investment/cash burning mode for a few years but is now finally on the verge of breakeven. I hadn’t contemplated that margin/profit hole when I made those 2019 estimates because a big podcast investment wasn’t on my radar. Notably, Premium gross margin is now over 29%, rising, and much closer to the 30.6% figure I’d estimated.

If Spotify was going to outperform in one area or another, I’m glad it did so with users and revenue. I think robust top line growth is the most critical indicator of future business value. The larger the company can be, the larger the ultimate free cash flows can be on a steady state basis once operations are fine tuned and optimized for profits. If Spotify had instead underperformed on users and revenue over the last four years—due to stronger competition?—but outperformed on margins and free cash flow, I would be much less enthusiastic about the future value of the business. Certainly, some cash flow would accrue to shareholders sooner, increasing the present value of the shares, but the ultimate size of the cash flows would be limited by a smaller than otherwise user/subscriber base. So I’m really pleased with Spotify’s performance since 2019 relative to my initial Base case assumptions. And if guidance is met, the business would almost reach my initial Bull case Premium sub number and would even beat my initial Super Bull case for total MAUs.

Revenue

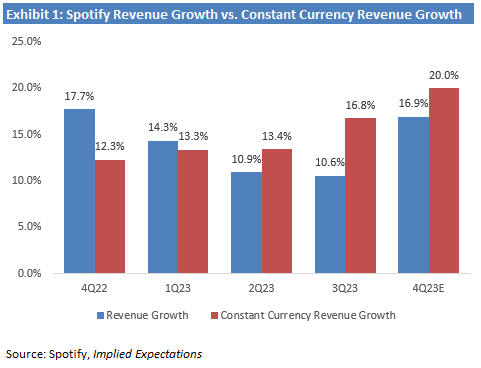

Revenue growth was 10.6% y/y, which is the 8th straight quarter of decelerating revenue growth. But looking under the hood at the impact of foreign exchange rate changes tells a different story. Constant currency revenue grew 16.8% y/y, the third straight quarter of accelerating revenue growth. As you can see, guidance suggests that continues to 20.0% constant currency revenue growth in the fourth quarter.

Gross margin expanded 166 bps y/y to 26.4%, ahead of guidance by 40 bps. Premium gross margin expanded 110 bps y/y to 29.1% while Ad-Supported gross margin went from 1.8% in the year-ago quarter to -5.7% in 2Q23 to 8.3% this quarter. Podcasting was only a small negative drag to overall gross margin and management expects it to hit breakeven in the short term and turn positive thereafter. That’s consistent with their comments at the 2021 Investor Day.

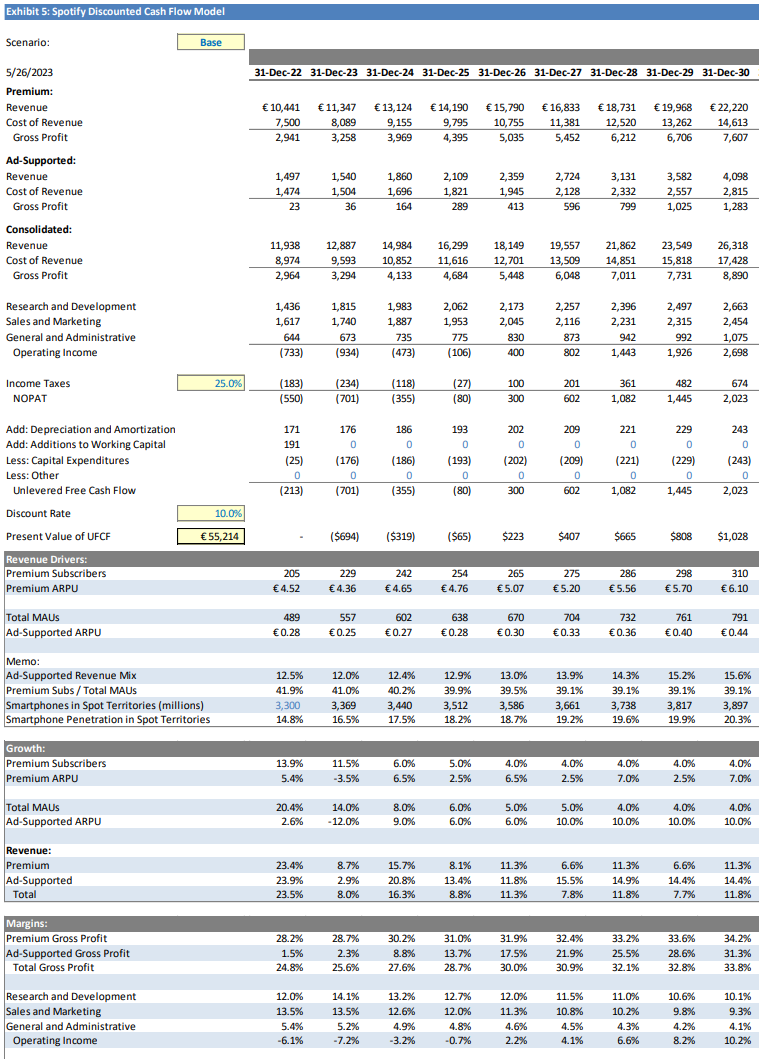

The opex efficiency might be the even bigger standout. In this screenshot from my model, you can see how much lower these expenses are as a percent of revenue this quarter.

The sales and marketing efficiency was particularly impressive. Sales and marketing declined €77 million y/y, primarily due to a €56 million decrease in advertising. Yet Spotify added 26 million MAUs this quarter, the same number as it added in the year ago quarter. Similarly, it added 6 million Premium subscribers this quarter, down only slightly from the 7 million in the year-ago quarter. Spotify’s customer acquisition costs certainly appear to be lower versus a year ago, continuing a trend that’s been in play each quarter this year. Daniel would say this is a reflection of the investments they have made over the years in the user experience, which drives engagement and retention, which lowers customer acquisition costs. It will be really impressive if this can continue.

The New Modus Operandi

Spotify has clearly changed its operating philosophy over the last few quarters. No longer is this a company that invests for growth at all costs. Daniel and Paul have gotten religion as it relates to efficiency.

Here’s Daniel on the call:

Here’s Paul on the call talking about this being an inflection point and the major change in the way they are now running the business:

Layoffs

On December 4th, Spotify announced a 17% reduction of its workforce.

While management had articulated there were more efficiencies left to come and there is a new modus operandi at Spotify, I was not expecting such a large workforce reduction so soon. Daniel is clearly taking this change in operating philosophy seriously.

As of September 30th, Spotify had 9,241 full-time equivalent employees. 17% of that would be 1,571 FTE employees. If they make on average $200,000 of total compensation and benefits, that would be $314.2 million of annual cost savings. That alone would represent a 2.4% bump to this year’s operating margin. On top of that, the company is also optimizing its real estate assets as a result of the headcount reduction, which should represent additional savings on an ongoing basis.

This really seems like a new company going forward. The fact that CFO Paul Vogel was then let go a few days later is even more striking. Daniel’s somewhat unusual statement basically suggested Paul does not have the skill set to be an efficiency-minded CFO.

I was surprised by that move and that statement. Most of the time, statements announcing the departure of an executive are worded to suggest the executive is voluntarily leaving to pursue other opportunities, even if that may not be exactly true. I guess this shows us how focused Daniel is on this new modus operandi.

Scenario Analysis

The last time I posted my scenario analysis and valuation of Spotify was in May. Here’s part of what my prior Base case assumptions spit out at the time.

With this update, I’m revising those MAU and Premium sub numbers higher to account for the healthier growth we’ve seen. Premium ARPU increases a bit to account for some price increases and management’s emphasis that pricing is now another tool in the took kit. Gross margin, particularly in the Ad-Supported business, improves at somewhat of a faster pace than I had previously assumed. And I’ve revised my opex assumptions lower for this headcount reduction and the new operating philosophy. I now have 2024 operating margin of 3.2%, up from -3.2%, and improving from there over time. The larger top line and higher margins sooner than previously expected are pulling free cash flows forward in time, boosting the present value of the business.

Here is the PDF of my scenario analysis and DCF work:

And here is my valuation summary in Euros, the reporting currency, using the business valuations derived in the PDF above:

And here is the same table translated into U.S. dollars, in which the stock trades:

For newer readers, the Priced In scenario is simply a reverse DCF. I tweak the long-term assumptions to back into a $196.15 per share intrinsic value, which matches yesterday’s closing price. There are of course countless combinations of underlying variables that would result in the same valuation, but this is one that seems plausible to me. Over the next 20 years, it assumes MAUs and Premium subs reach 892 million and 344 million, respectively. Those are both 2.1% long-term CAGRs. That MAU number is a huge miss from Daniel’s goal of 1 billion MAUs in a decade. This also assumes revenue reaches €25.8 billion in a decade and €40.7 billion a decade beyond that. That’s a 6.1% revenue CAGR. Operating margins reach about 11% in a decade and 17% another decade after that. Certainly, I think there is some growth and margin expansion baked in here. So if you are super stingy and don’t want to pay for any of that, I’m not sure this price should interest you.

Personally, I would call that a floor but we’ll see. I think it’s more likely that we reach and pass 1 billion MAUs and 400 million Premium subs over time. I think gross margins are on a path into the mid-30%s and ticking up from there over time. Opex is likely to get more efficient than anyone expected not very long ago. Based on those two things, my guess is operating margins can reach mid-to-high teens in a decade and a bit higher beyond that. Incremental gross margins on the Premium and Ad-Supported side were about 40% and 50%, respectively, last quarter, which are what I assume over the long-term. That’s how you get reported gross margins moving up, and that coupled with opex efficiency and operating leverage is how you get substantial operating margin expansion over time.

That said, it’s up to you to decide what you think. My scenarios are meant to answer the question, “What do I have to believe about Spotify’s future to think the stock is worth X today? What about Y? What about Z?” Some may find that a more interesting methodology than me slapping an arbitrary number on next year’s earnings or revenue.

Ek’s Warrants

Daniel still owns 800,000 warrants he bought from the company a couple years ago. They have an exercise price of $281.63 and expire this coming August. We’ll have to see if he can salvage any value out of these. SPOT would need to jump 44% from here for these warrants to start to get in the money and 67% from here for Daniel to breakeven, given what he paid for them. That would be a herculean eight months. Obviously, this is an irrelevant side show compared to his other 31.1 million shares that are worth $6.1 billion.

Conclusion

Spotify has been firing on all cylinders on the user and subscriber side. The multi-year podcasting drag on gross margins is finally fading away and should start to contribute positively shortly. And Daniel is getting some serious religion on efficiencies. Like he said, it’s time to turn this great product into a great business. They are now sustainably in the black on profits and on cash flows, both of which are poised to accelerate. There really isn’t much more I could ask of the business right now.

That said, there are undoubtedly higher expectations baked in at $196 per share than there were at $79 where we started the year. But at the same time, my valuations have also shifted higher given both the stronger growth, encouraging pricing power dynamics, and the meaningful pull-forward of profits and cash flows that are pretty clearly coming. With a fairly wide range of error in both directions, my best guess is the shares are still worth about twice what they’re trading for today. That would provide more than adequate forward returns from today’s price.

Disclosure: Long SPOT

Disclaimer: This post is for entertainment purposes only and is not a recommendation to buy or sell any security. Everything I write could be completely wrong and the stock I’m writing about could go to $0. Rely entirely on your own research and investment judgement.

Hi IE,

Just curious, how did you calculate Ad-supported ARPU of 0.28 in Dec-22?

Great work as always IE.

Sorry to hear about your dad, my condolences to you and your family.