Peloton: The Hardest Problem Is Already Solved

Peloton reported its fiscal third quarter yesterday morning. Here’s Barry McCarthy’s first shareholder letter:

https://investor.onepeloton.com/static-files/6fc0b035-ea15-4617-9558-8ebd348c1169

Barry McCarthy is an incredible executive. I can’t think of a better person for this job at this moment. It has been clear for a long time that he understands subscription business economics as well as anyone (watch his session from Spotify’s 2018 Analyst Day for a sense). He had impressive and highly effective runs at Netflix and Spotify. But aside from his resume, it is refreshing that he tells it like it is. He is hyper-rational. He sees things as they are, not how he wishes they would be. Instead of telling investors how great everything is regardless of the circumstances, he is up front about the problems the company faces and what they are doing to fix them. That establishes trust. When someone tells you the good, the bad, and the ugly, you have more confidence that you are getting the full story. That is not very common among public company executives, but it should be.

Here’s a good example from the shareholder letter.

Some of the challenges we face are systems related (there is substantial tech debt, not uncommon among successful fast-growing businesses) which tax our productivity and speed of decision making, as well as our speed of execution. And some of the challenges have resulted from poor execution, like last quarter’s increased use of 3PL partners for last mile distribution. The strategy wasn’t flawed, but our execution was. Better systems. Better decision making. Better execution. We’re working on it.

Peloton Interactive CEO Barry McCarthy in his F3Q 2022 Shareholder Letter

And here is him elaborating on the topic on the call.

Well, so let me tell the story this way. The business was crowdsourced so there’s a bunch of software that was hacked. The business started to have success. Like all tech companies I’ve ever been associated with, all of the resources of the business were focused on engineering and product in order to accelerate growth. And then COVID hits. And so the business explodes from 700,000 subs to 3 million subs. And all those systems-related issues are still present in the business today. So the order management system is still the original code that was hacked when the business was first organized. And pretty much all of that needs to be rewritten.

And then there are a bunch of downstream issues that happened because of the way that the order management system was architected and speaks to the — to all the accounting-related systems, the ERP system. And if you work in customer service, I think I’ve heard there are 13 or 16 different screens you look at in order to be able to see the entire customer history. And Andy has just hired a new head of customer service, and we’re going to be addressing some of those issues. So when you actually call up our customer service reps are actually able to be helpful because we’ve organized all that information on one screen. So those are kinds of — those are examples of some of the kinds of issues we face.

Others relate to our ability to push code in our engineering team and the productivity of engineers. This is an issue, for instance, in the last couple of years that Spotify very effectively wrestled to the ground. But even after it was public, it was an issue that they had to address, and we have to address it here as well. And so as a consequence, it slows down the speed at which we’re able to A/B test and the speed at which we’re able to update our e-commerce platform. You see that in our ability to quickly get to market to A/B test Fitness-as-a-Service, for instance. I mean, really, we have to wait until the end of June to be able to A/B test on the website? That’s something that would take a day and a half at Netflix, even early on. But it is what it is, and we’ll get through it.

We understand what the issues are now, and we’ll get the kind of expertise we need in-house to get it fixed. These are not unsolvable problems. They’re not problems that companies like us haven’t seen. We just have to get our arms around it and fix it. Then in 12 months, we’ll be in a much better place than we are today. So they don’t threaten the business. It just slows us down, and we move a little slower than we would like to as a consequence.

Peloton Interactive CEO Barry McCarthy on the F3Q 2022 Conference Call

I doubt we would have heard this from John. I give him tremendous credit for having the big idea and bringing it to life despite being laughed out of so many rooms when meeting with VCs. It takes a special kind of entrepreneur to forge ahead. And I thank him for probably extending years to my life. He was eternally optimistic, which worked well until it didn’t.

And our team is planning that and getting ready for it, again, trying not to get over our skis with the OpEx or the CapEx way too far in advance, but you’ve got to make some bets. And as always, we’re going to bet on success, not bet on failure because they kind of become self-fulfilling.

Peloton Interactive Founder and Chairman John Foley on the F4Q 2021 Conference Call

We now know that Peloton was already way out over their skis at that point, but didn’t realize it yet. To be fair, they are far from the only ones who appear to have gotten ahead of themselves with pandemic-related expansions.

The Quarter

Certainly, the negative hardware margins and cash burn were ugly. I wish raising the $750 million of term debt wasn’t necessary. But as a long-term thinker and Peloton shareholder, I thought this report was encouraging.

The good:

Peloton reported 194,951 Connected Fitness net adds, which nicely beat management’s guidance of 163,000.

Average monthly churn ticked down sequentially to 0.75%.

Monthly average workouts per All-Access subscription ticked up sequentially to 18.8.

I think a lot of investors, including me, were bracing for worse results than this. I had 160,000 net adds and 0.85% churn penciled in. I keep expecting churn to tick up due to the reopening but this is still a pretty normal, low level for Peloton. That said, I have always assumed it will tick up a bit over time.

For context, average monthly churn over the last five years has been as low as 0.31% during the height of the pandemic to 0.90% a few years ago. The average has been 0.65%.

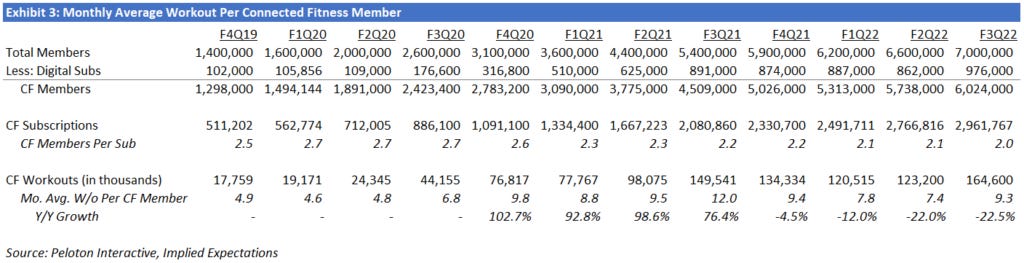

The primary reason churn is so low is the high engagement, which is of course driven by the great user experience as evidenced by the high NPS. That continued this quarter with the average Connected Fitness subscription averaging 18.8 workouts per month. As you can see this is down from the pandemic highs but still well above where it was pre-Covid.

Some of this quarter’s uptick is seasonal due to New Year’s resolutions. This is also not a per-person metric; it’s a per subscription metric and there’s an average of two members per All-Access subscription today.

In Exhibit 3, I back into how many workouts the average person on a Connected Fitness subscription is averaging. For those who don’t know, Peloton reports Members, which is anyone with a Peloton account, including those using household All-Access subscriptions or single user digital app subscriptions. It also reports Digital app subscriptions. So you can do the math to see that there are about 6 million CF Members on household All-Access subscriptions. You can divide that by CF workouts, which they disclose, to see that the average person on an All-Access subscription averaged 9.3 workouts per month this quarter.

While that’s interesting, I think churn is naturally more tied to workouts per subscription. Although it is not a linear relationship. If a subscription goes from 20 workouts per month to 15, the higher propensity to churn is immeasurable. If it goes from 5 to 1, it is measurable.

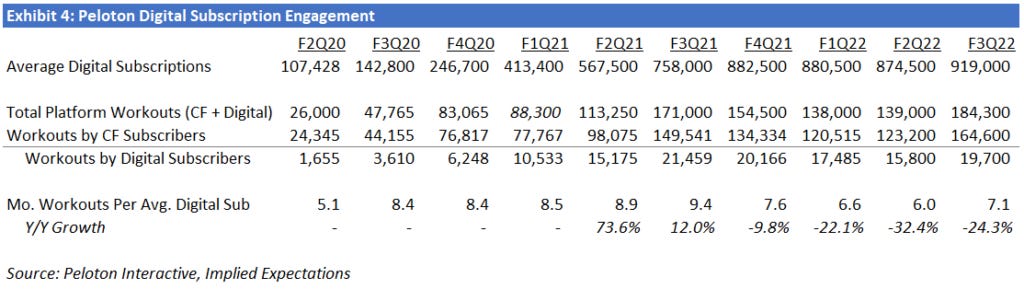

And here is monthly average workouts per Digital app subscriber, which shows the same sort of year-over-year decline comping against peak Covid but sequential uptick.

Not surprisingly, they work out a bit less frequently than the average person on an All-Access membership.

Subscription gross margin expanded 360 bps year-over-year to 68.2%. That’s an incremental margin of 74.7%. This is primarily due to continued fixed cost leverage, which is due to producing content that can be sold to a growing base of users.

Total revenue of $964 million was within the $950 million to $1 billion guidance.

The bad and the ugly: