Netflix: What's Priced In?

Netflix: What's Priced In?

Netflix is getting harder to value.

I published Netflix: Disanchoring two weeks ago and promised a follow up to provide some updated valuation thoughts.

Netflix is getting harder to value. I don’t mean the process is more difficult than it used to be. I mean the range of upside outcomes is becoming wider. It has always been hard to be precise but that is getting even harder.

Until recently, you could lay out long-term assumptions for subs and ARM by geographic segment. You could look at current broadband penetration rates and make assumptions for how they increase over time. While the future is always uncertain, that modeling was straightforward.

Now, with the November rollout of the Basic with Ads tier and the launch of paid sharing in March, this is an unusually uncertain time to be forecasting Netflix’s near-term (‘23 and ‘24) revenue growth. More importantly, it has also become more uncertain to be forecasting Netflix’s long run revenue growth due to the strong likelihood that the company develops a free ad-supported offering.

I wrote about the potential for a free tier in Netflix: Turning on the Spigots (July 2022) as well as in Netflix: Disanchoring. Other global content platforms that have compelling content and are free to the consumer are Facebook and YouTube. Each has closer to three billion global users. When you make something compelling that’s also free, adoption increases. No surprise. Look at YouTube. ~2.6 billion users and maybe 80 million Premium subscribers so far. YouTube Premium is still early but that is 3% paid penetration so far. Spotify’s Premium offering is more mature with 205 million Premium subs but that’s out of 489 million MAUs. Still 58%—the majority—are not paying. Netflix is 100% paid for now. But how many more household users would use Netflix regularly if it had a free offering? It has 231 million paying households today and ~331 million total household users including password sharers—could it easily have 600 million sometime in the future with a free ad-supported tier? 800 million? Maybe. That’s what I mean by Netflix is getting harder to value.

The good news for Netflix owners is the new developments seem to only make the range of outcomes wider to the upside, not the downside.

Paid Sharing and Basic with Ads

Management’s first-quarter guidance called for 4%-8% constant currency revenue growth, which should accelerate throughout the year. But “accelerate” can mean a lot of things.

Here’s how I’m currently thinking about it. We know there are 100 million or more global households that are watching Netflix using a paying member’s password, including 30 million in UCAN. How many of the paying members will opt to pay an extra $4 (?) per month for the extra member? And of those who decline to do so, how many of their freeloaders will sign up for their own accounts?

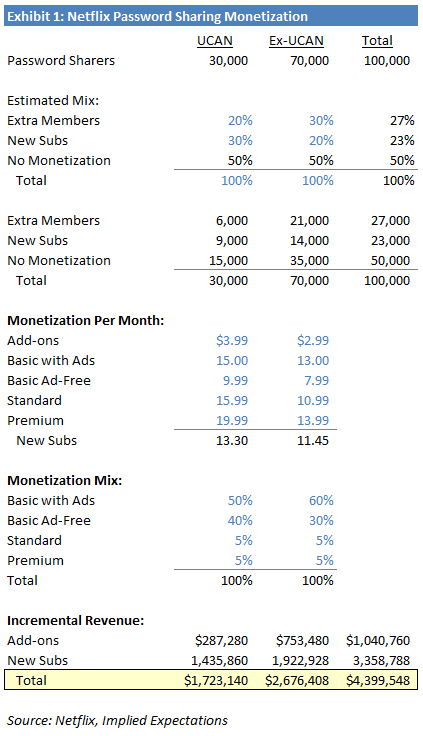

I took a stab at answering this question last April in Netflix: Monetizing the Freeloaders. Here is what I came up with at the time.

I now think I was a probably a bit low with 20% uptake of new accounts. A lot of extra members will come from parents who want to pay for their kid’s account at college or after. Friends or siblings currently sharing with each other will be less likely to pay extra for them. Some may want to venmo the $3-$4 to the account owner every month, which might be on top of whatever they might have been paying them already, which means the $6.99 ad-tier might suddenly be more attractive. And on the call, Greg made a comment that seemed to suggest a lot of password sharing isn’t about the money—they have the ability to pay—but they aren’t going to if they don’t have to.

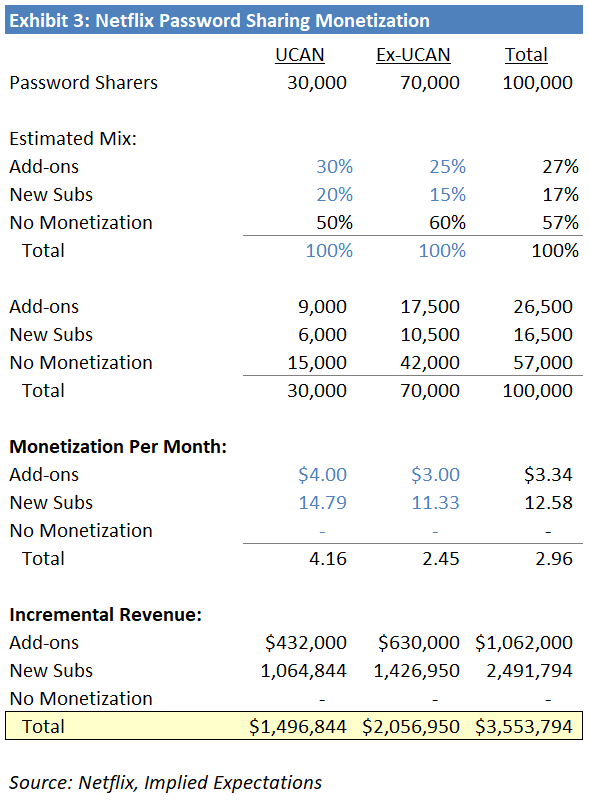

I updated the exhibit to lower extra member uptake from 30% to 20% and raised new subs from 20% to 30%. I also assume Basic with Ads monetizes better than Basic Ad-Free, but that $15 is still a lot lower than what I came up with in Netflix: Some Ad-Supported Math. Here’s the new version:

In that scenario, Netflix would get about $4.4 billion of incremental annual revenue globally, virtually all of which would drop to EBIT. I’d guess this might take a couple years to play out. But given the company’s EBIT was $5.6 billion last year, that would be quite meaningful. Obviously, I’m guessing and am definitely wrong to some extent but that could be in the ballpark.

I just saw a survey that polled password sharers on what they will do when the crackdown comes. 10% said the would sign up for Basic Ad-free, 12% said they would sign up for Basic with Ads, 16% said they would be willing to pay something to be on the existing account, and 62% said they would stop using Netflix.

Surveys about future behavior are notoriously unreliable. If you survey people whether they will cancel Netflix if they raise prices, a far higher percentage will say yes than actually end up canceling. Despite that, my exhibit above is not that far from those survey results. I plug in 50% for the percentage who would stop using Netflix, but even that may be too high in the long run, especially when the ad tier is only $6.99 per month.

In any case, which of those assumptions do you think might be wrong? impliedexpectations@gmail.com or post a comment below.

Long-Term Margins

I think the single biggest gap between my view and the implied expectations today relates to Netflix’s long-term margins. Netflix’s operating margins have been hovering around 20% lately due to the unexpected growth slowdown and currency. Prior to last year, they had been expanding operating margins at a 330 bps per year on average over the prior five years. My sense is people may be anchoring too much on margins around this level and not thinking enough from first principles about what really drives Netflix’s margins, where they could go long term, and why.

Most companies that grow revenue for a long time should be expected to scale opex. In Netflix’s case, Marketing, Technology and Development, and G&A should all see operating leverage and come down as a percent of revenue over time. That’s probably not too controversial.

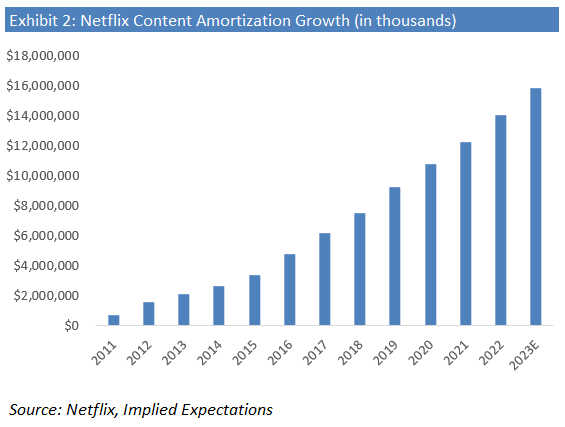

What may be most controversial is Netflix’s long-term gross margin expansion. The bulk of cost of revenue is content amortization. Netflix licenses and produces content on a fixed cost basis, which means means the cost of a given piece of content does not increase regardless of how many viewers watch it or how much subscriber and advertising revenue it supports. That allows for huge operating leverage as revenue scales. I think most investors understand that concept but may be underestimating how it could apply to Netflix over the long term. What clouds the issue is Netflix has ramped content spending for so long. Content costs hardly look fixed.

That looks pretty variable, right? The nuance is the underlying content deals are absolutely fixed cost deals, but Netflix had been layering so many more on top of each other year after year that content amortization has soared. As a result, most of the financial benefits of fixed cost content have not been allowed to shine through on Netflix’s P&L to any eye-opening extent yet. They got some benefit—330 bps of operating margin expansion per year on average from 2016 to 2021—but it was a measured pace. A managed outcome. And then that came to a halt last year as revenue growth underperformed, so investors are even less likely to imagine a future that is very different than the present.

I envision Netflix’s long-term mature operating margins being…