Netflix: Turning on the Spigots

I intended to shift to less frequent than quarterly updates of the usual suspects, but I just can’t quit writing about Netflix. That said, I intend these updates to be briefer than usual going forward because I’m devoting more time to studying other businesses that I’ll write about going forward. I’m all ears if you have suggestions for companies you think I’d find interesting: impliedexpectations@gmail.com.

Netflix reported its second quarter results Tuesday night. Here’s the shareholder letter. I’m not going to rehash it or the call but will instead focus on the analysis.

Big Picture

I think buying NFLX in 2022, down 75% from its highs, just as it is about to get more efficient as a business with headcount and content spending, and just before it gets into advertising and starts monetizing password sharing, will look very obvious in hindsight. But today, based on my read of sentiment, I feel like I’m one of the few with this point of view. Generally, I hear that Netflix’s business model is “broken” or “permanently impaired.” That it has so much competition that it’s gone “ex-growth” and churn will accelerate. Sometimes, I wonder if I’m looking at the same business.

Here are some facts. Netflix has 221 million paying subscribers globally who are paying an average of $11.96 per month. That is driving about $32 billion of streaming revenue this year. No other streaming service is close in revenue, engagement, or the ability to reinvest in content and technology. On top of the 221 million, there are another 100+ million unmonetized households enjoying the service for free… for now. That’s an unbelievable 45% of the current paying subscriber base.

As for going “ex-growth,” revenue just grew 13% on a constant currency basis and is expected to grow at similar rates for the rest of the year… before starting to accelerate next year due to password sharing monetization and the start of the new ad-supported tier. Rather than increasing, churn in the U.S. has decreased back down to near pre-price change levels.

Look at this engagement relative to peers. Engagement drives retention and pricing power in this business, which explains why Netflix has $32 billion and counting of streaming revenue.

So what exactly makes the business “broken,” “permanently impaired,” or “ex-growth?”

Certainly, subscriber and revenue growth has slowed. The company has lost 1.2 million subs year-to-date. But 0.7 million of them related to the voluntary exit of Russia. That means that Netflix has lost 0.5 million paying subs (out of 221 million) in the months after a double-digit percentage price increase (it always sees temporarily higher churn after a price increase), which was implemented in the midst of massive inflation in everything around us, and when payment itself is optional since users can easily watch for free with a shared password. Additionally, the war in Ukraine could be impacting EMEA while more competition on the margin and engagement headwinds from growing platforms like TikTok act as headwinds. Despite all this, Netflix’s paying subscriber count is likely to turn positive for the year ex-Russia in a few weeks given their third-quarter guidance of 1 million paid net adds. And it’s likely to be up for the full year even including Russia.

Now, of course being up single-digit millions of subs for the year is a far cry from prior expectations. Netflix clearly ran into a wall this year. The subscriber and revenue growth slowdown surprised the market and surprised management. While management’s initial view during 2021 was its paid net adds slowdown was due to a pull forward in demand from the pandemic, they abandoned that view earlier this year in favor of other reasons, including high connected TV penetration when considering the 100 million households that are password sharing, macro, inflation, competition, Ukraine, and of course the temporary effects of the January price increase.

But I still find the pull forward argument compelling. If you were going to sign up for Netflix, you would likely have done so when you were locked down at home during the pandemic. Paid net adds had slowed during 2021 until the fourth quarter when Netflix added 8.3 million subs, essentially on pace with the 8.5 million in 4Q20. That almost suggested the pull-forward slowdown was waning. But the following quarter in 1Q21 paid net adds slowed sharply, which coincided with Netflix’s price increase (11% in the U.S. and other increases globally) during a period of very high inflation. As a friend pointed out, the global synchronization of the paid net add slowdown suggests it was driven by macro-related factors affecting the whole world, ie. pandemic pull forward and/or price increases during a high inflationary environment when password sharing is easy, rather than something like competition, which is most meaningful in the U.S.

It would be perfectly rational for someone feeling the pinch of rising prices to cancel their now-more-expensive Netflix subscription when they can easily share passwords with a paying member. More people are more likely to do that during a period of high inflation than ever before. Why pay if you don’t have to?

I also think management failed to appreciate how much of the global connected TV market it had already penetrated when including the 100+ million households that are watching Netflix for free via password sharing. Of course, connected TV penetration continues to grow around the world, but 321 million households using Netflix, including the password sharers, might now be the majority of the current connected TV households ex-China.

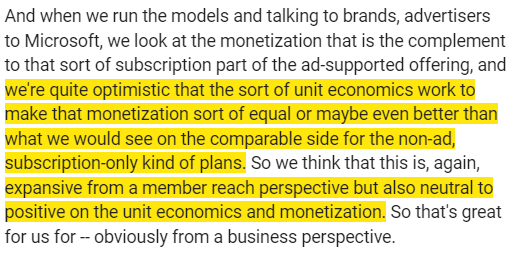

While connected TV penetration continues to increase over time towards 1 billion or more households ex-China, Netflix needs to do two things near term to get over this hump: 1) maximize monetization of those 100+ million password sharing households, and 2) roll out the cheaper ad-supported tier to bring in the more price-sensitive consumers, many of whom may be password sharing. Simply put, Netflix has to start getting paid for those 100 million and attract more subs via a lower-priced advertising tier. Importantly, considering the password sharers are not paying anything yet and the ad-supported tier should monetize as well or better than the ad-free plans, these two initiatives represent only upside, in my view.

I’ve taken a stab about how material these two initiatives could be financially in Netflix: Monetizing the Freeloaders and Netflix: Some Ad-Supported Math. Both seem significant and underappreciated to me. Obviously, the future is uncertain and my assumptions are sure to miss the mark, but the possible outcomes appear skewed to the upside to one extent or another.

As one would expect, management is bullish about them. COO Greg Peters had this to say about their password sharing monetization tests underway in Latin America as it relates to a global rollout:

And management believes, like others do as well, that Netflix ad inventory would garner premium CPMs. That is one of the contributing factors behind why the ad tier should monetize better than the ad-free tier. I went into some detail about premium CPMs, ad load, and engagement in Netflix: Some Ad-Supported Math.

While all the evidence suggested the ad-supported tier would monetize at least as well as the ad-free tiers, it’s good to hear management confirm that.

We can also see how bullish management is by focusing on their words rather than just their official guidance. Here’s CFO Spence Neumann discussing guidance for flat operating margins ex-fx and ex-restructuring through 2023.

Ok, so flat margins ex-fx until we reignite revenue growth. Yet at the same time, he’s saying they expect to reaccelerate revenue growth in 2023, which of course should start to ramp operating margins.

Basically, he’s strongly suggesting they’re going to reaccelerate revenue growth next year and in 2024, which should cause them to beat their flat margin guidance.

Content Spending Moderation + Revenue Acceleration = High Operating Leverage

Given management’s comments in the letter about the cash content spending to amortization ratio coming down to 1.2x-1.3x this year, content amortization should be between $13.1 billion and $14.2 billion this year. Cash spending should remain around $17 billion for the next “couple or few years” while that ratio declines towards 1.0x, meaning content amortization would inch higher towards $17 billion over the next few years.

These content spending figures are… (subscribe for more)