Chipotle's unit economics and reinvestment opportunity make this a business worth understanding despite its recent troubles.

The unit economics, especially for new units, were steadily improving through the end of last quarter.

Management is now pulling out all the stops via accelerating menu innovation, television advertising, digital ordering, as well as testing drive-thru, family meals, grab-n-go options, and in-vehicle pick-up.

Chipotle Mexican Grill is very controversial in the investment community. On one hand, it has a long history of creating enormous shareholder value and has what appears to be a long runway ahead. On the other hand, the business has been significantly harmed by food safety incidents and the recovery has been disappointing thus far.

In this report, I will do three things.

I will explain what makes Chipotle so interesting despite its recent struggles.

I will outline the company’s origins and recent history.

I will discuss the company’s initiatives to recover its historic unit economics.

What Makes Chipotle So Interesting

Chipotle is a great business with a long growth runway that is currently struggling to recover from food safety and reputational problems. The same circumstances applied to almost any other restaurant chain would not interest me. What interests me about Chipotle and what separates it from other restaurants is its stellar unit economics. Unit economics are the returns the company generates from operating its restaurants. Chipotle's unit economics are excellent, even at today's depressed sales levels, and the company has the opportunity to open thousands more restaurants in the U.S. over time and generate excellent incremental returns.

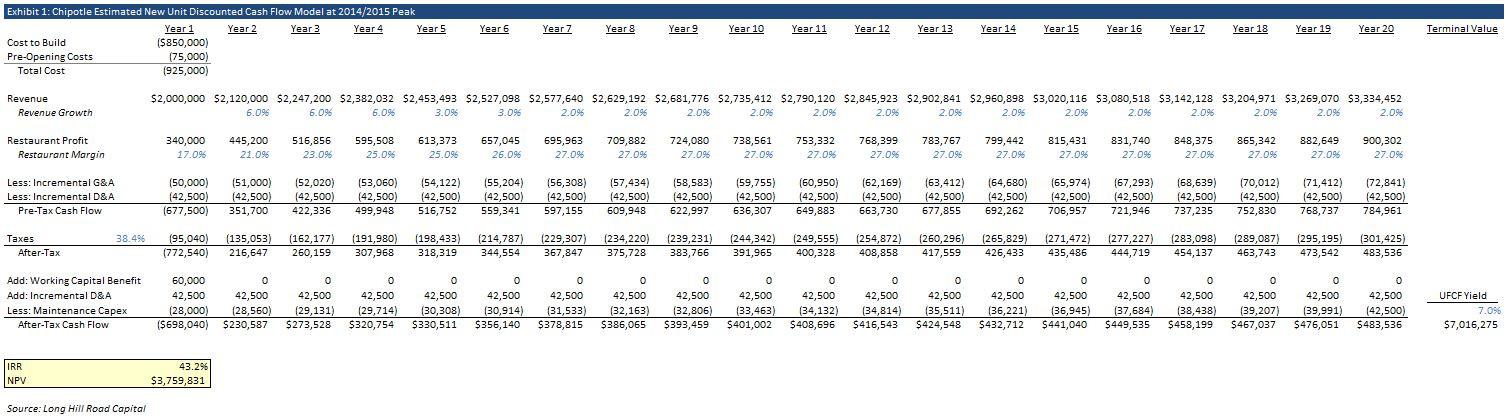

Prior to the food safety events of late 2015, Chipotle would spend about $850,000 net of landlord reimbursements to open one new restaurant and, within a few years, it would be making over $300,000 of after-tax cash flow annually. That was phenomenal and best-in-class among restaurants. The company would recover its entire new store investment often in less than four years (the “payback period”). I estimate the net present value (“NPV”) of a new store was approaching $4 million. In other words, Chipotle appeared to be creating close to $4 million of shareholder value every time it opened a new store. This value creation machine and the prospects for thousands of additional restaurants caused the market to ascribe the stock with a $23 billion valuation at its peak in 2015.

Exhibit 1 (click to enlarge) shows my NPV analysis of a new Chipotle unit opened in 2014. Of course, those units have underperformed this model given the food-safety debacle, but this is roughly what investors were expecting from new units at the time.

My current analysis of Chipotle's new unit NPV shows new units are still quite value-accretive but less so than a few years ago.

Company Origins and Recent History

Steve Ells graduated from the Culinary Institute of America and worked as a sous chef at the Stars restaurant in San Francisco. He aspired to open his own fine dining restaurant, but could not afford it yet so he decided to open a more modest venture in the meantime. Having been inspired by the Mexican fare in San Francisco’s mission district, Ells opened his first Chipotle in Colorado in 1996. This project was meant to allow Ells to make and save enough money to open a fine dining restaurant, but the concept was so popular that he opened several more. Eventually, McDonald’s acquired an interest in Chipotle and used its real estate expertise to help accelerate Chipotle’s unit growth. By the time of Chipotle’s IPO in 2006, the brand had 489 restaurants across 22 states. McDonald’s sold its investment in the IPO and shortly thereafter.

From the 2006 IPO to late 2015, Chipotle’s unit count went from 489 to 1,895 and average unit economics improved over the years. The stock went from $22 per share at the IPO to a pre-food safety high of $758 per share in late 2015, a mind-boggling 34-bagger in under ten years. The driver was the 1) already great but continuously improving unit economics, and 2) earning fantastic returns opening over 1,400 new restaurants over that period.

Chipotle ran into trouble in late 2015 when hundreds of customers fell sick from eating at Chipotle. Cases of E. coli, salmonella, and norovirus were the culprits. The financial impact on the company has been devastating. During the first quarter of 2016, same-store sales declined by 30% and restaurant margins fell from 27.5% to 6.8%. Trailing twelve month average restaurant sales fell from $2.5 million to $1.9 million at the low point. The company’s stock fell from the $700s to the low $400s for most of last year.

Since then, the company has been working to recover its former unit economics. Despite additional marketing and food giveaways, the recovery has been far less robust than most people expected. A separate norovirus incident at one Virginia Chipotle in July of 2017 has not helped, causing enough bad publicity to send the stock spiraling down to as low as $296 per share in August. Today, the stock trades near $320 per share.

The post-food safety bull case for Chipotle's stock has largely relied on historical case studies of other restaurant chains that recovered from E. coli outbreaks. McDonald’s in 1982, Jack in the Box in 1993, Burger King in 1997, KFC in 1999, and Taco Bell in 2006 are some prominent examples. To varying degrees these incidents created weak financial results initially but in each case the restaurant chain recovered over time as the news faded from headlines and customers returned to their normal habits.

Many thought that pattern would repeat with Chipotle, but its recovery to date has meaningfully lagged the case study recoveries. The different recovery trajectories are likely due to the speed at which bad news travels today over social media and 24-hour cable news. These media outlets largely did not exist during the case study outbreaks. That explains how Jack-in-the-Box had a more robust recovery in the early-to-mid 80s from a far worse outbreak (four children died) than Chipotle has had thus far from its issues (no deaths).

Despite the lackluster recovery thus far, Chipotle remains a tremendously popular brand. Only a handful of quick-service or fast casual restaurant brands can claim $2 million of average unit volume, and few, if any, competitors can touch Chipotle's economic model.

Through the end of the second quarter, Chipotle’s same-store sales have returned to growth. First and second-quarter comps rose 17.8% and 8.6%, respectively. Sell-side analysts focus on this metric as well as the "two-year stacked comp," which is a geometric progression that shows performance compared to the same quarter two years ago. That can be interesting but is also of limited use because comparing results to the same quarter two years ago is an arbitrary and moving target. For example, those looking at the two-year stack in 2016 were comparing to 2014, which wasn't the peak AUV period yet (until 4Q). And starting in the fourth quarter of this year, the two-year stack will be comparing to fourth-quarter 2015, which was the start of the food safety crisis when results were well-off peak. So the two-year stack doesn't compare results to a constant benchmark and is therefore of limited use.

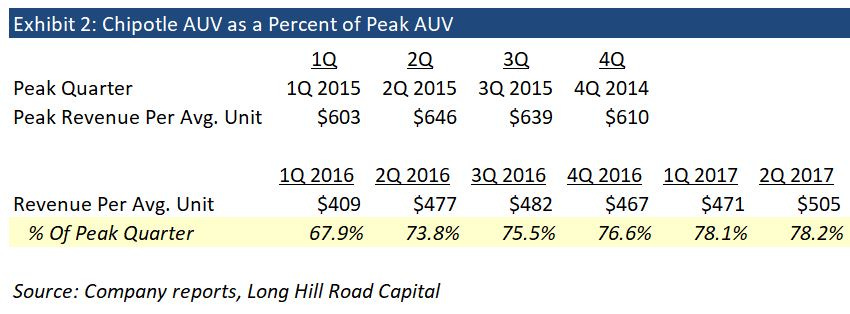

My approach is to compare quarterly AUV levels against peak AUV levels. The peak 1Q was 1Q 2015, the peak 2Q was 2Q 2015, the peak 3Q was 3Q 2015, and the peak 4Q was 4Q 2014. We will always be able to compare any quarter's AUV to those peak periods and have a clear and sensible comparison showing how far along we are in recovering towards peak AUV.

So where is Chipotle today compared to peak AUV?

As you can see from Exhibit 2, Chipotle has made slow and steady progress. 1Q 2016 started at about 68% of the peak 1Q level and that has climbed to about 78% of the peak 2Q level in 2Q 2017. Certainly, CMG bulls wish progress was faster but things have been going in the right direction.

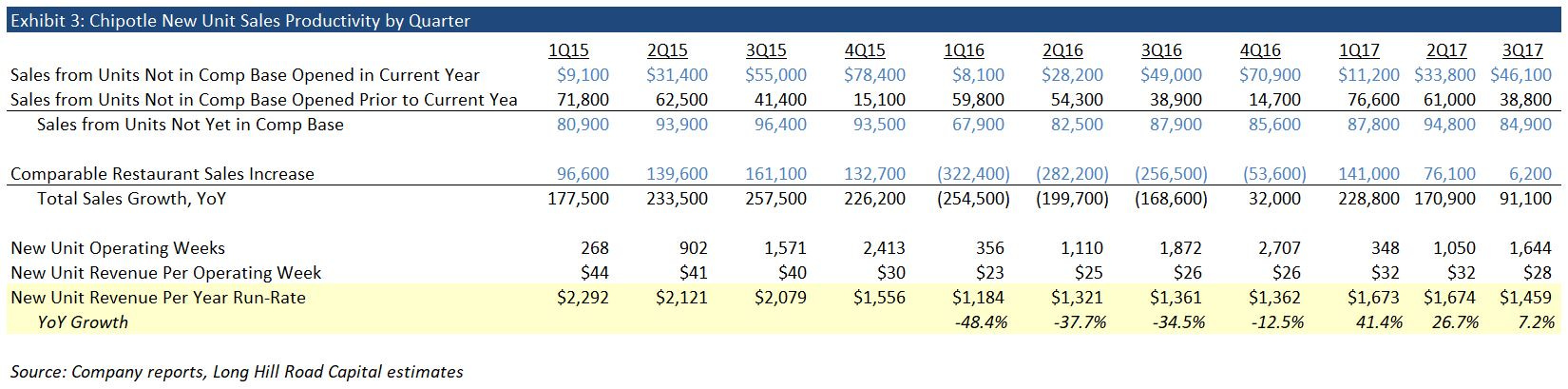

Another important sign of progress is the recent improvements in sales at new units. To understand this one needs to analyze the following table from the 10-Qs and 10-Ks.

The blue highlighted section is where the key information lies. Exhibit 3 shows my analysis of this disclosure over the last two and a half years.

As you can see, in 2Q 2017 there was $33.8 million of sales attributable to restaurants that were opened in 2017. There were also about 1,050 new unit operating weeks during the quarter (new units * weeks they operated). Dividing $33.8 million by 1,050 suggests new units averaged $32,000 of revenue per week or a run-rate of around $1.674 million per year. That is 26.7% higher than the $1.321 million run-rate in 2Q of 2016. That is important progress because the returns that Chipotle generates on new units drive a large part of the company’s long-term value.

How does $1.3 and $1.7 million compare to the prior peak levels for new unit productivity? One has to dig through the company’s proxy statements to answer that. The proxy statements show the four metrics that drive executive compensation, the targets for each metric that were set for the prior year, and in several years, the actual numbers achieved. One of the four metrics is “new restaurant average daily sales.” Exhibit 4 shows the targets set forth at the start of each year and either the actual figures achieved or the commentary provided.

As you can see, peak new unit productivity was achieved in 2014 when new units averaged an annual run-rate just under $2.0 million. With new units now operating near a $1.7 million run-rate, the company’s new units are actually performing reasonably well; only the 2013-2015 period achieved higher new unit productivity. Still, Chipotle has an opportunity to continue to close that gap, and doing so would create tremendous shareholder value.

Importantly, I do not believe Chipotle’s recent progress with new unit productivity is well-understood. Management recently alluded to improving returns on new units but it was a vague, off-hand remark without evidence provided. To gain that insight, one needs to not only read the filings but also think critically about the disclosures and perform separate analysis. In my experience, most market participants, professional or otherwise, tend not to do that.

Recent Initiatives and Tests

Chipotle is now pulling out all the stops in order to recoup its historical unit economic model. This is a company that had such stellar business results for so many years that it did not feel the need to develop new menu items, advertise in any meaningful way, drive digital sales, or even focus on the guest experience.

For a store to achieve the high-performing “Restaurateur” status, the company used to score restaurants based on a complex set of “esoteric concepts and abstract measures,” few of which directly impacted the guest experience. After Steve Ells took over sole CEO duties in December of 2016 (the company had two co-CEOs previously), he cited the fact that half of the company’s restaurants were earning a “C” or worse grade in terms of their internal guest experience metrics. As a result, the company overhauled the Restaurateur program such that it now focuses on five direct and measurable factors that directly impact the guest experience. Since making these changes, store employees now have more time available for training, hiring, marketing, and customer service. Chipotle is seeing decreased employee turnover, better customer service scores, better digital sales support, and labor efficiencies. In fact, General Manager turnover is now at the lowest level it has been in more than 8 years.

Chipotle is also undergoing another big evolution. After a largely static menu and limited advertising for its entire corporate existence, Chipotle has changed course. Management now recognizes the need for something new and fresh at Chipotle, to change the public dialogue about the brand and drive traffic to the restaurants. It is now testing several new menu items, including at a new dedicated test kitchen store called Chipotle NEXT in New York. There customers can find two new desserts, an citrus avocado dressing, and new margaritas to name a few. Queso, a Mexican cheese sauce for those unfamiliar, made it through the test kitchen and select test markets and was rolled out nationally in September.

The company’s marketing strategy has also changed. It used to produce animated shorts showcasing where food comes from and similar food themes, and other forms of inexpensive but effective marketing. Now, the company is advertising heavily on television. In addition, the company’s mobile and online ordering initiatives now gives it the ability to identify specific customers and their visit frequency, and target them individually with specific promotions. The company can now more quickly identify marketing campaigns that work well and change course as needed.

Chipotle is also innovating with online and digital ordering. This is a large opportunity for the company. As of earlier this year, fast-casual competitor Panera Bread said that 26% of its sales were through digital channels (mobile, online and kiosk). Pizza competitors generally get half of sales through these channels. During the second-quarter, Chipotle saw online orders increase 52%, mobile orders increase 37%, and catering orders increase 9%. These orders increased to 8.5% of company sales in the quarter. The company has a long runway to increase that towards the 26% level that Panera is achieving. Why is that important for Chipotle? Customers who order digitally skip the line, pick up their waiting orders, and walk out. One of Chipotle’s “problems” is its uniquely long lines, which highlights the brand’s popularity, but also turns off many customers who are unwilling to wait 20 minutes. To the extent Chipotle can increase digital orders, it should alleviate congestion on the lines and allow more customers to join the line, leading to increased sales.

The company is also picking up its catering business. Historically, customers would have to call the store and place an order over the phone. That is simply a bad experience for the customer and it unnecessarily occupies an employee’s time. Now, customers can order catering online and even have it delivered in an increasing number of stores. During the second quarter, 1,000 stores began offering catering delivery and management planned to roll it out to more stores later this year. Catering sales are very attractive for two reasons: one, they are very high ticket orders, and two, they have high incremental margins.

Chipotle is also testing a variety of new customer service mechanisms. They are about to open a new restaurant in Ohio that has a drive-thru window. Drive-thru is a big opportunity because it significantly increases average unit volume. Starbucks has cited a 40% increase in sales for new units that open with drive-thrus versus units without drive-thru. Panera’s founder Ron Shaich has estimated that about half of drive-thru sales are incremental; in other words, half are from customers who would not have walked in the door. If drive-thru increased Chipotle’s units volume by even 20%, it would drive the average unit’s volume from around $2.0 million to $2.4 million, which alone would get it back to near-peak AUV levels from 2014.

Unfortunately, not all of Chipotle’s locations can be retrofitted with drive-thru. According to the 10-K, 1,396 locations are end-cap locations, 370 are free-standing, 346 are in-line, and 138 are some other type (food court, airport, etc.). I would assume most of the free-standing locations and a portion of the end-cap locations could be retrofitted with drive-thru. It is also possible Chipotle will add drive-thru capabilities to many of its new units. It will be very interesting to hear how the Ohio store test goes.

Interestingly, the locations that cannot offer drive-thru could have an alternative solution. On the second-quarter conference call, Steve Ells referred to “in-vehicle pick up” as something they are exploring. He did not elaborate on that term, but I can only assume it means the customer can place a mobile order and a Chipotle employee will run the order out to the customer’s car when they arrive. Perhaps the store could have geolocation targeting so they can tell exactly when the customer arrives, which would be highly-efficient for the store and also very pleasing for customers. I know my family would order more Chipotle if we did not have to get the kids out of and back in the car just to pick up take out.

Management is also testing smaller sized catering orders, family meals, and grab-n-go options. Outside of "Food With Integrity," there are no longer any sacred cows at Chipotle. Management is testing anything and everything to see what will maximize sales and margins as quickly as possible.

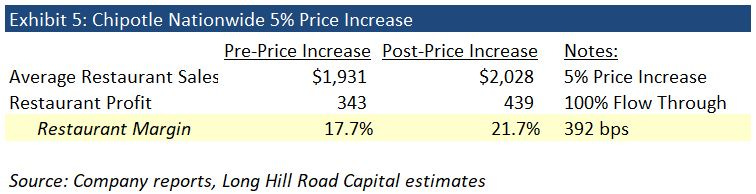

Pricing Power

Over the years, Chipotle has not raised its menu prices in line with the food cost inflation it has endured. Food, beverage, and packaging expense as a percent of sales went from 30.6% in 2010 to 35.0% last year. Chipotle’s menu is now underpriced for what it is, in my opinion. I can buy a chicken burrito or burrito bowl for $6.80 plus tax where I live, and the portion size is usually enough for two meals. When I eat at other fast-casual restaurants nearby, I typically spend over $9 and sometimes up to $11 for what is a one-meal portion size.

Management recognizes this and finally increased prices 5% at 440 units in April and by 4-5% at the 60 New York restaurants in May. This was about 22% of the store base. Chipotle has historically seen little to no resistance to price increases and this time was no different. In my judgement, management strongly hinted at another wave of price increases to occur during the current fourth quarter. Whether that occurs shortly or not is beside the point though. Chipotle is likely to raise prices nationally over the next year or so, and this is likely to have a surprising positive effect on same-store sales and restaurant margins. Exhibit 5 shows first-quarter average restaurant sales, which was before the first wave of price increases, restaurant profit, and restaurant margins, and the impact of a 5% price increase, all of which drops to profit. As a result, I believe a nationwide 5% price increase would increase total company restaurant margins by almost 400 basis points, all else equal. I believe it is only a matter of time, and I think this is widely overlooked and underappreciated.

Final Thoughts

Chipotle’s saga is a case study in crisis management, disaster recovery, and public relations. The company has missed the mark on several of these items and its recovery has been disappointing thus far. But many of the company’s initiatives appear promising, the brand’s popularity remains largely intact, underlying unit economics have been slowly improving, and the stock is trading at a fraction of its former high. Chipotle is a fascinating business and one worth our attention given its unit economics, the potential for improving unit economics, and its long unit growth runway.

If you haven't already, I'd suggest reading my more quantitative report on Chipotle that includes scenario analysis, discounted cash flow models, new unit NPVs, and suggests buy prices from which investors would do very well.

Disclosure: Long CMG