Carvana: Liquidity, Retail Units, and GPU

Carvana: Liquidity, Retail Units, and GPU

What should we consider about the key variables going forward?

There is a lot to discuss about Carvana, but the elephant in the room is its cash burn and liquidity situation. Nothing else matters for now and probably for the next 12-18 months. In this post, I’ll touch on their primary liquidity resources and some of the key variables that will determine the outcome for investors. To be clear up front, this is absolutely not a recommendation to buy or sell any security.

Liquidity Situation

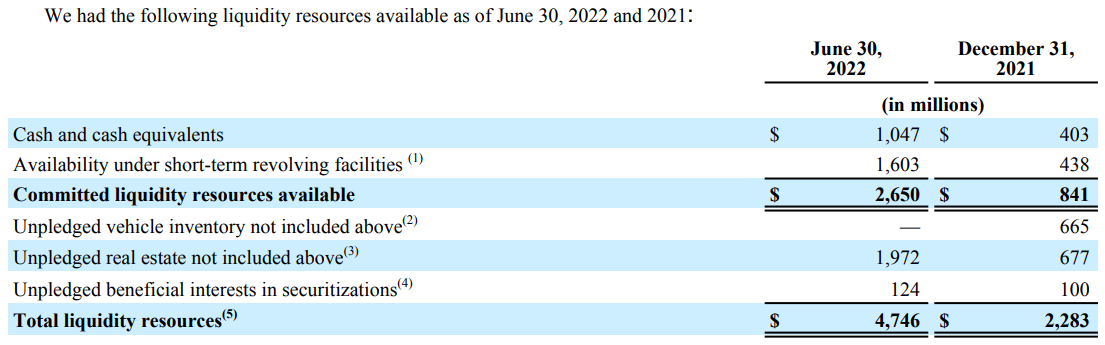

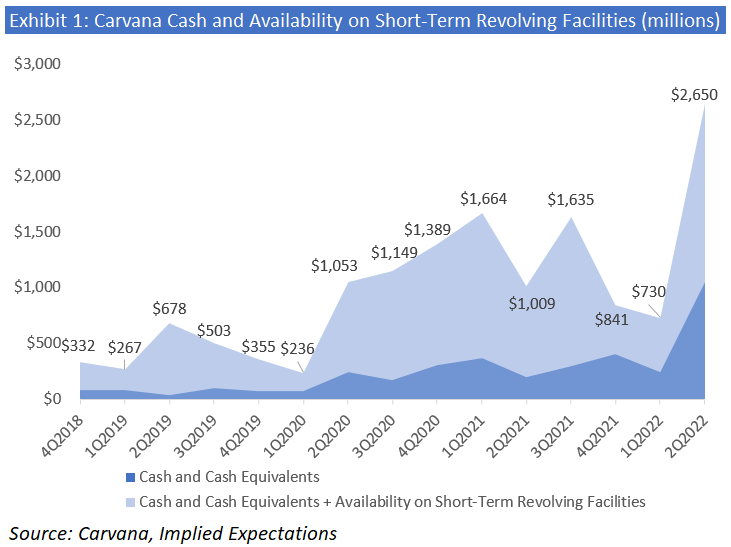

As of June 30th, the company had $2.65 billion of cash plus availability on its Floor Plan and finance receivable facilities. There is also another $2.0 billion of unpledged real estate assets and $0.1 billion of unpledged beneficial interests in securitizations. I think we can have confidence in the $2.65 billion—management is able to draw on and pay down these facilities with excess cash to minimize near-term interest expense, so it is all available to them. But I would not necessarily count on the company being able to monetize the unpledged real estate or interests in securitizations in the near term.

$2.65 billion of cash and revolver availability is by far the most committed liquidity resources Carvana has ever had. That may not be the impression one gets from looking at the stock chart.

This all-time high cash and committed revolver availability is the result of issuing 15.6 million new shares at $80 per share in April, which raised net proceeds of $1.2 billion, and issuing $1.075 billion of 10.25% debt beyond what they needed to acquire ADESA in May. The original intention of the latter was to fund reconditioning capacity expansions at ADESA’s auction sites over time. But given the company already has 1.2 million retail units of annual capacity at full IRC staffing and is expected to have 1.4 million by year-end—versus the 400,000-425,000 retail unit sales run-rate at the moment—there is no urgency to spend that capital on further capacity expansions for the time being. Minimizing cash burn and getting to cash flow breakeven is management’s highest near-term priority. So practically speaking, the $1.075 billion is being used for general corporate purposes, ie. to absorb cash burn.

The key questions are, “Can the company get to self-funding with $2.65 billion of cash and committed liquidity resources? How long will it take to get there? How long will the liquidity resources last? What is management doing to extend its runway and get to EBITDA ex-SBC positive first and ultimately to cash flow positive? And what are the key variables to consider going forward?” Clearly, the market is skeptical, rightly so.

Carvana is a company that has been growing so fast that it routinely invests in and builds out its infrastructure 6-12 months ahead of expected demand growth. And for most of its existence, it has been growing retail units at a triple digit annual pace. When the used car market hit the “affordability wall” this year—with both used car prices and auto loan rates soaring—having a cost structure built for far more demand than showed up resulted in a huge spike in cash burn in the first quarter.

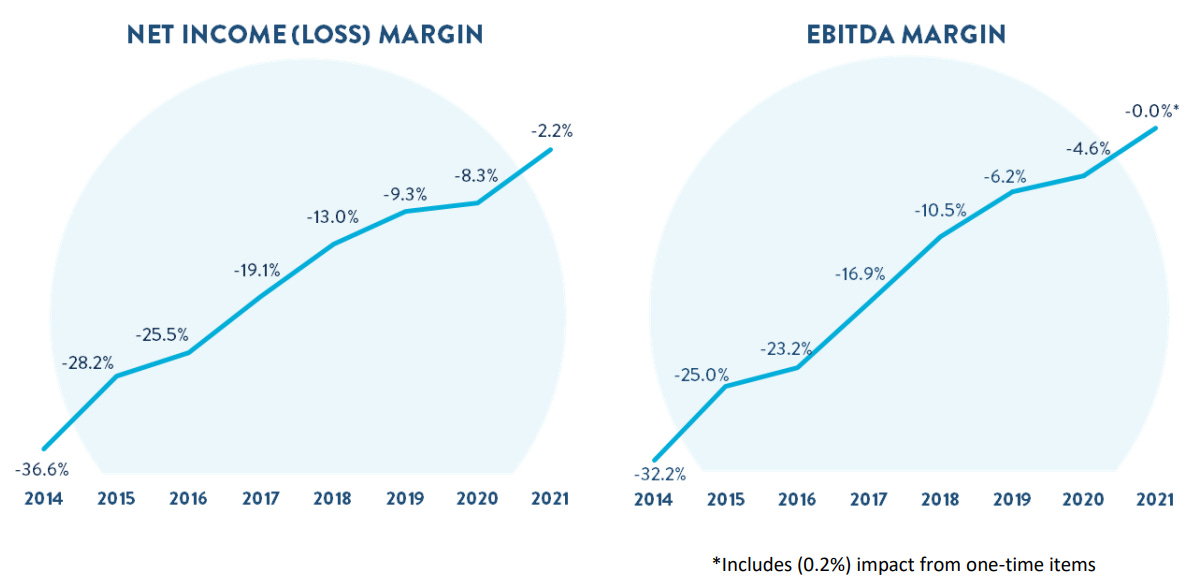

I think it’s important to point out the context. As you can see below, Carvana’s deeply negative margins in its earlier days have significantly improved as the company has scaled over time to near-breakeven last year.

Last year, it burned only $82 million of core free cash flow (before inventory and receivables, which are financed) and even achieved positive net income for the first time in a quarter. This was despite always prioritizing growth over efficiency. The first quarter spike in cash burn put a swift halt to this progress, and together with the expensive cost of debt to fund ADESA, put the company’s liquidity runway in question.

In May, management pivoted from all-out growth mode to all-out efficiency mode. All hands have been on deck since. Layoffs occurred. Employees who had been tasked with maximizing growth are now tasked with maximizing efficiency. This is a massive cultural pivot and it won’t be easy. The goal is to first get to adjusted EBITDA ex-SBC positive—where core free cash burn would be mostly interest expense and capex—and eventually to free cash flow positive.

Regarding the liquidity runway, the result will primarily depend on these three variables over the next 12-18 months:

Retail units sold

Gross profit per unit (“GPU”) ex-D&A and ex-SBC (“Cash GPU”)

SG&A per unit ex-D&A and ex-SBC (“Cash SG&A per unit”)

So what are these, why do they matter, and what should we expect from them going forward?

Cash GPU minus Cash SG&A/unit equals “Cash Contribution Per Unit.” The following formula…