Carvana: Feedback Loops

On Thursday of last week, Carvana raised its outlook for its second quarter. Ernie spoke at the William Blair conference on the same day to explain.

Second-quarter adjusted EBITDA increased from “positive” previously to “above $50 million” while non-GAAP GPU went from “above $5,000” to “above $6,000.” The “majority” of the non-GAAP GPU improvement is the result of selling down a large chunk of the elevated backlog of loans during the quarter. The “majority” language that Ernie used at the conference seemed to imply a minority of the improvement was attributable to something else, likely better retail GPU as a result of falling average days to sale.

Bears and skeptics point out the non-recurring nature of the loan sales, which is, of course, correct. Carvana could have either sold down the loan backlog quickly, in which case there would be a brief surge in Other GPU, or more gradually, in which case Other GPU would remain somewhat elevated for a longer stretch. Carvana chose the former as market conditions have been favorable.

But pointing out non-recurring nature of the loan sales to try to suggest meaningful progress isn’t being made is missing the forest from the trees. Of course non-GAAP GPU should normalize lower from this second-quarter spike as the pace of loan sales normalizes. But so what? Carvana doesn’t need to sustain greater than $6,000 non-GAAP GPU to be successful. $5,000 or greater, which I think will be a sustainable level, would be fantastic in conjunction with non-GAAP SG&A per unit likely falling below $5,000 this quarter and eventually below $4,000. Again, the spread between non-GAAP GPU and non-GAAP SG&A per unit can be called cash contribution per unit or adjusted EBITDA per unit. Multiply that by retail unit volume and we have adjusted EBITDA, which while not at all true cash flow can be considered the key building block towards it.

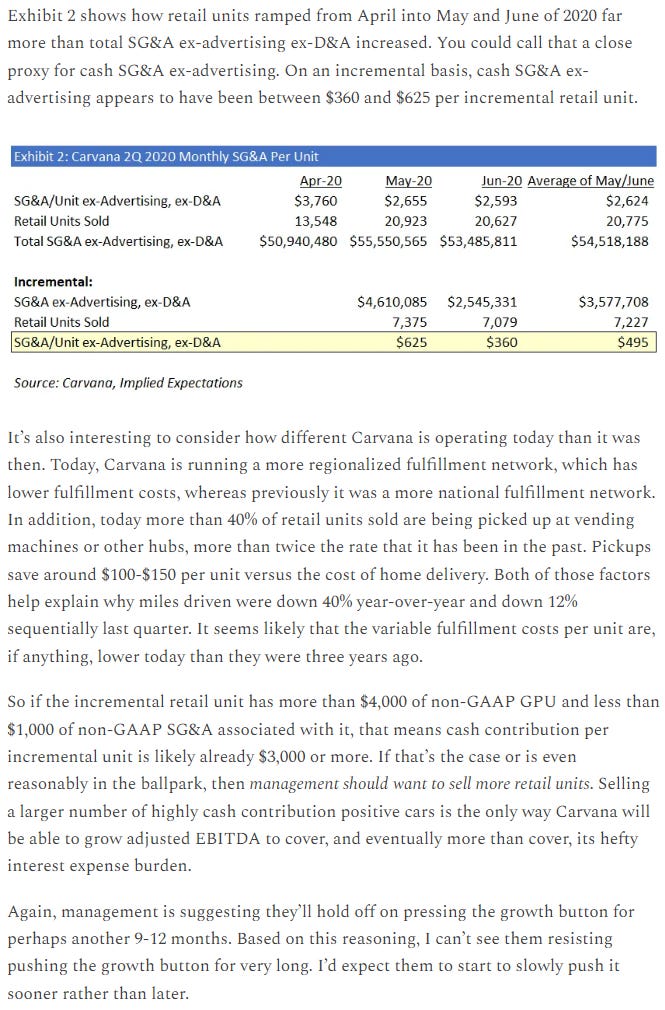

In the second quarter, I think we might see something like $6,250 of non-GAAP GPU and around $4,900 of non-GAAP SG&A per unit ($391 million / ~79k retail units), down from $5,098 in the first quarter. That would drive about $1,300 of cash contribution per unit. That should take a step back in the third quarter as loan sales normalize, dropping non-GAAP GPU to perhaps $5,000 while non-GAAP SG&A per unit might drop to around $4,400 ($360 million / 82k retail units) as the second-half cost cutting program bears fruit. That still would be more than $600 of cash contribution per unit and $50 million of adjusted EBITDA.

Beyond the third quarter, I think non-GAAP GPU can continue to tick up with a bit more volume running through the underutilized (~30% capacity utilization) fixed cost infrastructure. The cuts to non-GAAP SG&A will probably be close to complete by then, so I therefore expect management to be starting to turn up the growth dials. Again, while volumes are not entirely in management’s control, they absolutely have meaningful influence over them, which I discussed in Carvana: Illuminating the Path (June ‘23):

And at this conference, Ernie made the comment:

I think his point is that there is way more demand for cars from Carvana than they are fulfilling today, which is partly due to self-inflicted profitability initiatives. They offer the best used car experience in my view yet only have 1% national market share. I think he’s saying they can fulfill more demand when they want to—by increasing inventory selection, increasing advertising, and generally pulling on the growth levers they shut off over the last year. My sense is even some Carvana bulls are too concerned about retail volumes because few seem to sufficiently appreciate that their volumes are depressed not only by macro affordability factors, which should only improve as used car prices continue to normalize lower, but meaningfully by the self-inflicted headwinds, which management can and will start to reverse when ready.

Retail units ticking up would drive down non-GAAP SG&A per unit. I could see cash contribution per unit rebounding to something like $900 in the fourth quarter. And at that point, the incremental unit economics are just too attractive to delay growth any longer, especially as most of the SG&A cost cutting will be behind them. In Carvana: Illuminating the Path, I wrote how the incremental unit economics already seem very attractive:

At the William Blair conference, Ernie acknowledged that the incremental unit economics are already attractive enough to justify stepping on the growth gas:

Feedback Loops

Ernie has talked about the positive feedback loops in the business that benefit the company as it scales. He’s also talked about how those went into reverse when the business shrinks as it has been over the last 12-18 months.

All those headwinds have contributed to the company’s decline in retail volumes. But the underlying business is the same as it was before and will get better with scale again when they return to growth:

On top of that, Carvana is as efficient as it’s ever been, which means it won’t be too long before growth drives real and meaningful profits for the first time ever. While they will continue to invest for growth, I don’t think they are going back to the old way of all-out growth mode where they acquire sales at any cost. And let’s not forget that even in all-out growth mode with less efficient operations than they are running today, they were improving adjusted EBITDA margins by almost 500 bps annually due to the inherent operating leverage in the business.

Further, there is clearly a detailed plan in place for returning to growth:

Model

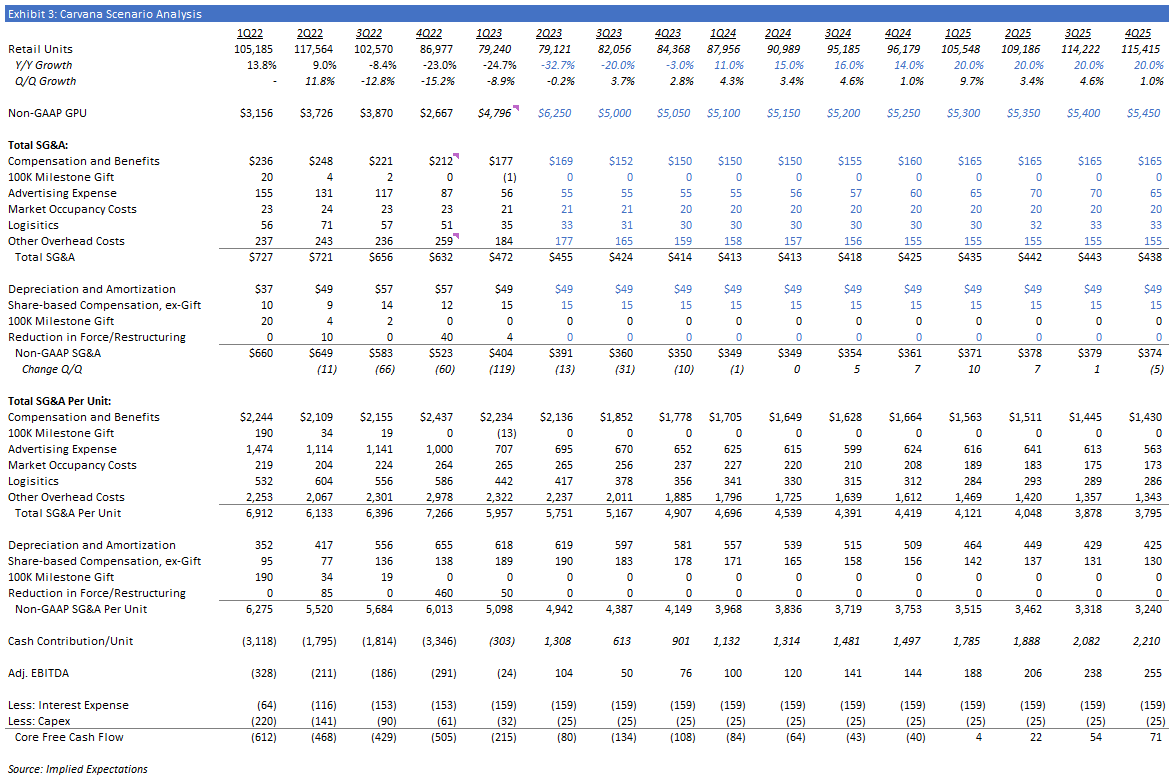

Here’s what I currently have penciled in for my revised base case through 2025:

As you can see, non-GAAP GPU jumps to $6,250 this quarter before normalizing to $5,000 in the third quarter and then slowly ticking up over time. Declines in non-GAAP SG&A are fairly moderate in the second quarter before picking up again in the third quarter and then generally leveling out. Retail unit volume is down slightly in the second quarter and modestly higher sequentially in the third and fourth quarters before accelerating a bit into 2024 and to 20% year-over-year growth in 2025.

I don’t think these assumptions are at all aggressive. In fact, if anything, I’d say retail unit volume growth of 14% in 2024 and 20% in 2025 should be conservative. By next year, I expect Carvana to be into Step 3—returning to growth. And my read of Ernie is that he considers Step 3 returning to “Carvana-like” growth. I think of that as 40%+ unit volume growth. So there is certainly room for better results than I’m penciling in at the moment.

What’s more, even with these assumptions that, if anything, are conservative, Carvana will generate adjusted EBITDA of $502 million next year and $885 million in 2025. That would drive core free cash burn down to $234 million in 2024 before Carvana would start generating positive core free cash flow in early 2025. That is still before stock-based comp but a) that’s irrelevant for a liquidity analysis and b) Carvana should leverage that over time.

Compare that to current consensus expectations:

Three observations. First, $22 million this quarter is below management’s guidance of greater than $50 million. This is now the third consecutive time the consensus refuses to bake in management’s near-term guidance. Second, consensus then has adjusted EBITDA falling negative again for the following three quarters. Frankly, I would be shocked if that happened. Between average days to sale crashing, which is meaningfully helping GPU, the momentum on the SG&A cutting side, and stable-ish retail volume at worst, I find that very unlikely. Third, consensus for this year is at -$8 million of adjusted EBITDA versus my $202 million, next year is at $106 million versus my $502 million, and 2025 is at $312 million versus my $885 million.

The sell-side is simply way behind the curve on Carvana. Between the business headwinds, the widespread liquidity concerns, short-term oriented buy-side clients who they talk to all day, and the lack of any career incentive to stray from the herd, sell-side analysts just do not want to recommend CVNA as an investment right now. And raising adjusted EBITDA numbers to anything more realistic would call into question that conclusion. When CVNA is $80 again, some of them may start to warm up to it.

Big Picture

I’m surprised CVNA is only trading at $23 and change as I write this given the fundamental improvements that are undeniable. This is binary. If Carvana emerges from the woods with acceptable levels of equity dilution or better, the stock is a clear multi-bagger from here over time. And with every business update we get, it looks increasingly likely to me that they will do exactly that.

For me, the ride from $3 and change per share to around $9 was “the hard money.” The risks and uncertainties were much higher. They had not yet shown the huge improvements in SG&A. Buying at $4 required some blind faith. In contrast, I think of the ride from $9 to $100+—or now from $23 to $100+—as the easier money. I don’t want to say “easy” but the liquidity risks were the only thing that could have stopped Carvana from getting back on the path to 2+ million retail units per year. And if you’re paying close attention, the probabilities of that have skyrocketed.

I used to think management would issue equity at the first opportunity, but then I realized that they were completely confident and comfortable internally with their plans and therefore probably wouldn’t. That’s why they did not entertain the idea of including equity in any debt exchange talks they had with their bondholders. They simply shot for better, more flexible terms on their debt but weren’t willing, and didn’t feel it necessary, to dilute the equity. There was no downside to trying—unless you include causing a general misinterpretation of the attempt at a debt exchange as a sign of weakness.

I’m not saying issuing equity is off the table. They probably should do so at some higher price. But I don't think they are interested in doing so at prices this depressed given their expectations for what’s to come. If the business plays out anything like I expect, there should be further meaningful surprises to the market to come. The short interest that’s 45% of the public shares and a substantial majority of the true float should only contribute to that. By the way, the Kerrisdale short report was atrociously bad, which the market very quickly sniffed out.

I’ll leave you with Ernie’s final comment from the conference:

Disclosure: Long CVNA

Disclaimer: This post is for entertainment purposes only and is not a recommendation to buy or sell any security. Everything I write could be completely wrong and the stock I’m writing about could go to $0. Rely entirely on your own research and investment judgement.

This article was incredible. Any updates coming?