Amazon: Mother of Other Bets

Is it Day Two at Amazon?

Amazon’s third-quarter report on October 27th showed net sales grew 15% year-over-year to $127.1 billion (+19% on a constant currency basis). The reported growth figures for each revenue line item are in the right column while constant currency growth figures are in the Q3 2022 column.

On the surface, this looks like a really nice sequential acceleration for most of these businesses. For example, online stores sales growth had been stuck in the -1% to 3% range for four quarters, but accelerated to 13% ex-currency. Unfortunately, that is flattered by Prime Day falling in 3Q22 this year while it fell in 2Q21 last year. That boosted year-over-year growth by 400 bps—a $4.4 billion tailwind to total revenue.

Amazon doesn’t break out Prime Day’s effect by line item, but allocating that tailwind pro-rata to online stores, 3P, and ads would suggest those lines would have grown something like 2%, 13%, and 19% year-over-year, respectively, on a reported basis. Then further adjusting out the currency headwind, they would have grown about 8%, 17%, and 24% on a constant currency basis, respectively. In other words, the reported growth rates are actually pretty close to the underlying growth rate once we strip out the Prime Day tailwind and the currency headwind. See Exhibit 1 for the math.

That’s still generally an acceleration, but not quite as impressive as it might seem at first glance. It was also boosted by a much easier comp. Recall CFO Brian Olsavsky said that mid-May was when pandemic-related comps got much easier for the e-commerce business. That means 3Q was the first full quarter with the easier comps.

4Q Guidance

Amazon’s stock sold off as much as 12% the day after it reported. Part of that was due to fourth-quarter guidance that called for just 2% to 8% year-over-year net sales growth. Excluding the 460 bps of expected currency headwind, that would be 6.6% to 12.6% underlying net sales growth. On the surface, that looks like a big slowdown relative to the ~18% ex-currency growth in 3Q, but I don’t think it is because, again, the underlying 3Q growth seems closer to 12% growth ex-Prime Day and currency.

Furthermore, Amazon has a long history of reporting actual net sales closer to the high end of its guidance range. The data behind Exhibit 1 shows that from 2001 through today, Amazon’s actual quarterly net sales growth has come in at 94% towards the high end of its priori guidance range.

So 4Q may not show that much of an underlying sequential slowdown. Or at least, not nearly the slowdown that the market may have initially thought management was guiding to. That could be why the market initially sent Amazon shares down 12% before rebounding slightly to close down less than 7%.

The other disappointing factor at play was the worsening margin at AWS and the largest single quarterly loss in the International segment’s history. More on this later.

Advertising

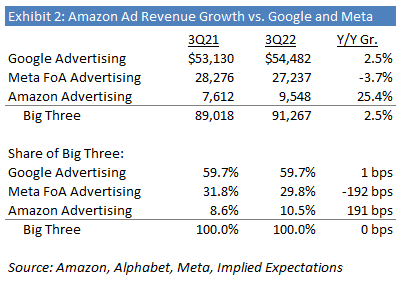

However you slice it, the ad business continues to show impressive growth—an estimated 24% ex-Prime Day, ex-currency—especially considering the environment. To put that in some context, Google’s ad business grew 3% last quarter and ~8% ex-currency. Meta’s Family of Apps ad revenue declined 4% and grew 3% ex-currency.

Certainly, Amazon’s ad business is less mature than that of the other two. It is also less impacted by Apple’s ATT changes it introduced last year, which is likely helping its growth relative to others.

Google’s ad business is still almost six times larger than Amazon’s while Meta’s is almost three times larger. At a high level, it’s incredible that Amazon created an ad business only about a decade ago, more or less—and didn’t even truly break it out separately in its reports until this year—yet it’s already more than one-third of Meta’s entire ad business. Exhibit 2 puts the big three digital ad businesses in context.

It’s also interesting to compare Amazon’s advertising revenue with its own advertising expense. In Exhibit 3, you can see how advertising net sales has grown to significantly exceed its own spending on advertising and other promotional costs. Assuming ad sales has a ~50% operating margin, one could say Amazon sellers and vendors are funding Amazon’s entire advertising budget across all its business units, including e-commerce, AWS, Prime Video, and everything else.

Finally, I went back to the archives to see what I wrote about Amazon’s advertising business in late 2014 when I first looked at and invested in Amazon.

It is always illuminating and humbling going back in time to see just how wrong I was about long-term expectations. I conservatively valued Amazon’s ad business at $2 billion or ~2x revenue at the time. Assuming a 50% contribution margin on sales and an 8% discount rate, the present value of the advertising cash flow stream since I wrote that through 2022 alone—assuming no terminal value—would be something like $37 billion. I was only too low by a factor of 16 even assuming the ad business disappeared after this year.

On one hand, it’s ok to be that wrong when being wrong actually benefits you as a shareholder. The ad business was a free option that paid off. But on the other hand, if you underestimate something by that much, the risk you face is you own too small of a position given the opportunity. Rob Vinall of RV Capital wrote something to the effect of, “Being conservative with forecasting shouldn’t be the goal; being accurate should be.” I agree with that and disagree with it at the same time, if that’s possible. I think it comes down to whether you are more focused on capturing upside or avoiding downside. What is the greater risk—owning too small of a position in a stock that ends up being a multi-bagger when you would have owned a large position had your forecast been accurate instead of conservative? Or owning too large of a position in a stock that gets permanently impaired when you would have only had a small position if your forecast hadn’t been way too optimistic? The key consideration in answering that is, of course, your forecasting skill. If you’re usually right about these things, then focusing on being accurate and capturing the upside might make more sense. If your forecasting ability is hit or miss, then focusing on being conservative and avoiding the downside might be the better approach.

Margins

Amazon’s margins were pretty low in the third quarter. North American margins…

[You’ve read about 40% of this post so far.]