Amazon: An Updated Valuation

Converting a series of long-term assumptions into a series of present values

Scenario Analysis

Compared to my last published version, I’ve made the following revisions (to my Base case unless otherwise noted):

North America and International revenue growth assumptions have come down to reflect this year’s slowing growth and slightly more modest longer term expectations. Both are now growing at a 7.0%-7.7% CAGR over the long term versus ~9% previously. These segments are Amazon ex-AWS and therefore include all sorts of different business lines.

AWS growth assumptions have also ticked down from 33% this year to 30%, from 28% next year to 23%, and so on. The long run CAGR goes from 13.2% to 12.6%. This is incremental conservatism more than anything else.

North America and International margins are lower near-term to reflect losses in 2022 and more modest near-term assumptions in the next few years, but are still expected to expand to 17.0% longer term as growth slows, the business gets more efficient, and there is a mix benefit towards higher margin ad sales. Amazon is clearly working hard to get more efficient as noted in recent press reports.

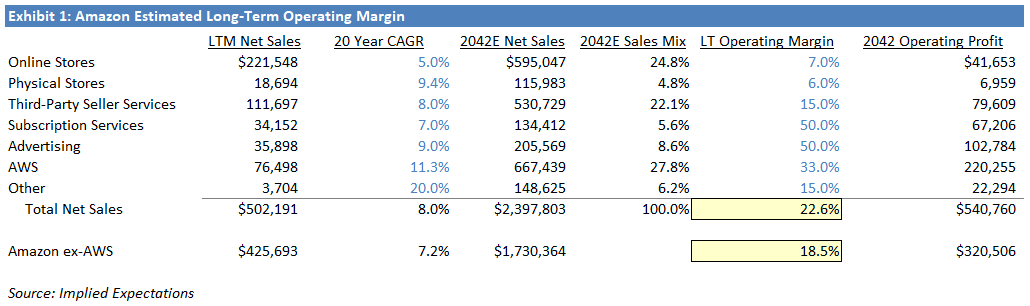

It would not surprise me if many think 17.0% long-term EBIT margins sounds aggressive. Exhibit 1 shows one way they could exceed that, but of course, the future is hard to predict. I’d love to hear good reasons why something like this is misguided.

AWS long-term incremental margins ticked down modestly from 37.5% to 37.0%. The larger impact is the reduced long-term revenue assumption noted above, which results in lower AWS EBIT in the long run than previously expected.

Here is the PDF that includes the long-term scenario analysis and six different DCFs (paid subs to IE with Models see a link to the downloadable Excel model—let me know if you’d like to upgrade: impliedexpectations@gmail.com):